Context

- The article argues that the rupee’s recent weakness cannot be explained only by external shocks or conventional macroeconomic indicators.

- Source: “The rupee’s problems run deep. RBI’s actions cannot stem its slide”, The Indian Express, April 19, 2026.

Historical Pattern of Rupee Stress

- External Triggers: Past sharp rupee declines were usually linked to global shocks such as the 2008 global financial crisis, the 2013 taper tantrum, energy price shocks after the Russia-Ukraine conflict, and the recent war in West Asia.

- Usual Domestic Explanations: High inflation and persistent current account deficit have often been cited as domestic reasons for the rupee’s depreciating bias.

- Present Shift: The article argues that factors beyond these conventional explanations are now weighing more heavily on the rupee’s near one-way decline.

Why the 2025 Rupee Fall Appeared Unusual

- Dollar-Rupee Divergence: From January to December 2025, the dollar index fell from 108.09 to 98.25, yet the rupee weakened from 85.70 to 89.91 against the dollar.

- Minority Trend: While the rupee weakened, many other currencies strengthened against the dollar, including the Thai baht, Chinese yuan, Korean won, Taiwanese dollar, Brazilian real, Mexican peso, euro, and pound; the Indonesian rupiah and Vietnamese dong were the other exceptions.

- Macro Mismatch: This happened during a so-called “Goldilocks phase” when growth was healthy and inflation and current account deficit were lower than historical trends.

- Core Argument: These macro indicators did not justify a roughly 5 per cent fall in the rupee when the dollar itself was weakening, indicating deeper country-specific pressures.

Capital Outflows as the Central Explanation

- Primary Driver: The article traces the rupee’s fall mainly to capital outflows.

- Trade Relations Factor: Deterioration in India-US trade relations dampened sentiment.

- Technology Factor: Absence of a domestic AI play reduced India’s attractiveness at a time when global investors were moving towards tech firms elsewhere.

- Domestic Flight of Capital: Domestic capital was also moving abroad in search of better opportunities.

- Growth-Confidence Link: These country-specific factors raised doubts over India’s growth prospects, leading to outflows and currency pressure.

- Important Distinction: Pressure on the rupee due to capital flows had already emerged before the war in West Asia.

Impact of the West Asia Conflict in 2026

- Risk Aversion Channel: With conflict in West Asia, investors became more risk averse and moved towards safety.

- Dollar Strengthening: The dollar index rose from 98.25 at the beginning of January 2026 to 100.59 by end-March.

- Further Rupee Weakness: During the same period, the rupee fell from 89.97 to 94.65.

- RBI Response: The article notes that exceptional steps by the central bank were needed to contain the rupee’s slide.

Can the Rupee Stabilise Again?

- Historical Comparison: In earlier episodes such as the 2013 taper tantrum, the rupee eventually stabilised after a steep fall.

- Conditional Relief: A possible Iran-US agreement could cool energy prices and reduce pressure on the current account.

- Incomplete Remedy: Even if energy market dislocations ease and trade with West Asia normalises, the article doubts whether capital flows will reverse automatically.

- Core Concern: If capital was leaving because of weakened confidence in India’s growth prospects, easing external tensions alone may not restore inflows.

Limits of RBI Intervention

- Short-Term Support: RBI interventions, including in the offshore NDF market, may provide temporary relief.

- Structural Constraint: Such steps are presented as unlikely to produce lasting stability if the core problem is investor confidence and persistent capital outflows.

- Main Conclusion: The rupee’s problems are deeper than temporary external shocks, so central bank action alone may not be enough to halt depreciation.

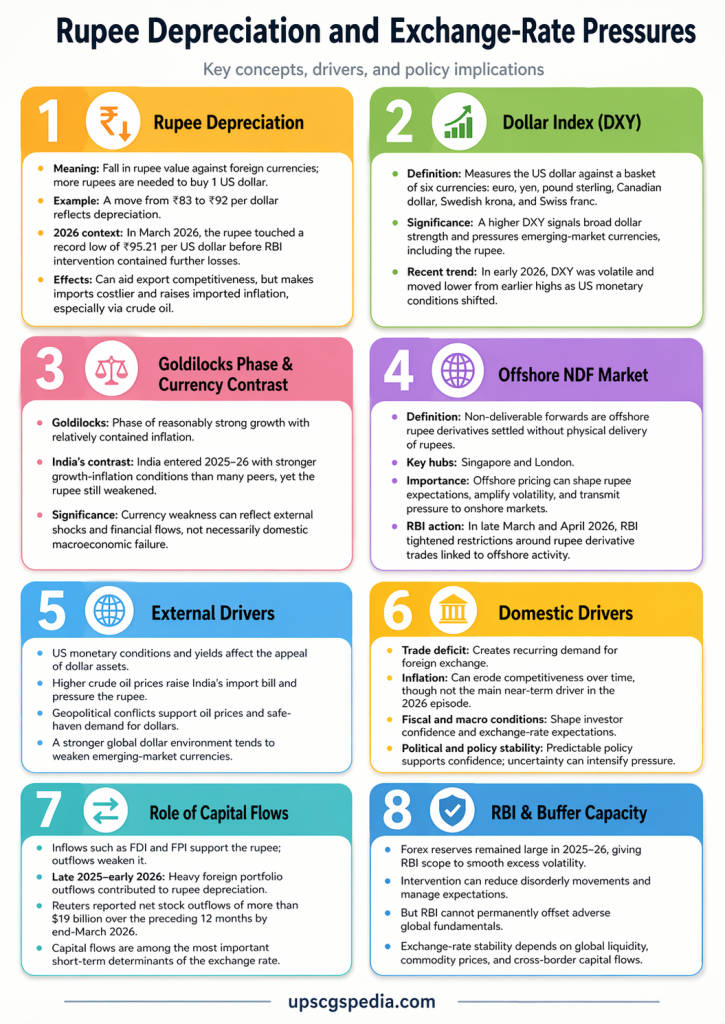

Indian Rupee In Early 2026

Rupee Depreciation

- Meaning: Rupee depreciation means a fall in the Rupee’s value against foreign currencies under market forces.

- Basic Mechanism: It means more Rupees are needed to buy one US Dollar.

- Early 2026 Movement: The Rupee came under sharp pressure in early 2026, fell to record lows, touched 92.63 on March 18, and weakened beyond 94 on April 23; markets also discussed the possibility of a move past 95.

- Immediate Triggers: The main near-term pressures were rising crude oil prices, war-related uncertainty in West Asia, and foreign capital outflows.

- Economic Effect: A weaker Rupee can improve export price competitiveness, but it also raises the domestic cost of imports, especially oil.

- Inflation Link: Costlier imports can transmit imported inflation into the economy, particularly through fuel and related channels.

Dollar Index (DXY)

- Meaning: The Dollar Index measures the strength of the US Dollar against a basket of six major currencies.

- Constituent Currencies: The basket includes the Euro, Japanese Yen, British Pound, Canadian Dollar, Swedish Krona, and Swiss Franc.

- Weight Pattern: The Euro carries the highest weight in the index.

- Analytical Importance: A stronger Dollar tends to put pressure on emerging-market currencies as investors move towards dollar assets during uncertainty.

- 2026 Relevance: In early 2026, global risk aversion and oil-linked uncertainty supported the Dollar and weakened Asian currencies, including the Rupee.

Goldilocks Phase

- Meaning: A Goldilocks phase refers to a macroeconomic situation of strong growth with relatively low inflation.

- Official Usage: The Government described late 2025 as “India’s Goldilocks Moment: High Growth, Low Inflation.”

- Growth Indicator: Real GDP growth reached 8.2% in Q2 FY 2025–26.

- Inflation Indicator: CPI inflation softened to 0.71% in November 2025, down from 4.26% in January 2025.

- Key Insight: The Rupee weakened even amid favourable domestic macro indicators, showing that external shocks could outweigh internal stability in exchange-rate movements.

Offshore NDF Market

- Meaning: The offshore Non-Deliverable Forward market is a derivatives market for the Rupee in which contracts are settled without delivery of physical Rupees.

- Policy Relevance: The RBI treated offshore derivative activity as a channel affecting Rupee volatility and imposed restrictions on April 1, 2026.

- Nature Of Restriction: Banks were barred from offering Rupee NDFs to clients under those temporary curbs.

- Subsequent Change: The RBI withdrew these offshore derivative restrictions on April 20, 2026, though uncertainty persisted in the market.

- Analytical Significance: The episode showed that offshore currency derivatives had become an important transmission channel for exchange-rate expectations and volatility.

External Drivers Of Rupee Pressure

- Crude Oil Prices: Higher oil prices worsen India’s external balance and raise demand for Dollars because India is heavily dependent on imported oil.

- Geopolitical Tensions: Conflict in West Asia and shipping tensions in the Gulf added to currency and market stress.

- Global Risk Aversion: In uncertain periods, investors prefer safer dollar assets, which puts pressure on emerging-market currencies.

- Fed And Global Financial Conditions: Global interest-rate expectations continued to shape capital allocation and currency behaviour, even when domestic fundamentals remained relatively stable.

Domestic Context

- Growth Resilience: India retained strong growth momentum despite a difficult global environment.

- Relative Weakness Of Rupee: Despite strong domestic growth, the Rupee remained one of the weaker regional currencies in 2026 because of energy vulnerability and weak capital flows.

- Core Interpretation: The Rupee’s fall in early 2026 did not by itself indicate domestic macroeconomic failure; external shocks played the dominant role.

Role Of Capital Flows

- Basic Role: Capital flows are one of the most important short-term drivers of exchange-rate movements.

- Inflows: Foreign investment inflows support the Rupee because they increase the supply of Dollars entering the domestic market.

- Outflows: Foreign investor exits weaken the Rupee because they increase Dollar demand and reduce support for domestic financial markets.

- 2026 Pattern: Foreign portfolio investor selling remained a major pressure point; Reuters reported about $8 billion in outflows from Indian stocks after the Iran war began and record FPI selling of $19.69 billion in FY2026.

- Wider Market Impact: Continued foreign outflows also weighed on Indian equities and broader sentiment in April 2026.

Overall Assessment

- Main Conclusion: The Rupee’s weakness in early 2026 was driven mainly by oil prices, geopolitical tensions, offshore currency volatility, and foreign capital outflows rather than by a collapse in domestic growth conditions.

- Broader Lesson: Exchange-rate movements can remain adverse even during a high-growth, low-inflation phase when global shocks and financial flows turn unfavourable.

UPSC Prelims Quiz

Practice exam-oriented current affairs questions daily and track your preparation effectively.

Attempt Quiz →