The Sixteenth Finance Commission has outlined a comprehensive framework for centre–state fiscal relations, resource distribution, and structural reforms for the period 2026–27 to 2030–31.

Constitutional Status And Legal Framework

Constitutional basis of the Finance Commission

The Finance Commission is a constitutional authority established under Article 280 of the Constitution. The President is required to constitute it every five years, or earlier if deemed necessary.

The Commission comprises a Chairperson and four other members, with Parliament empowered to determine their qualifications and mode of appointment.

Mandate under Article 280(3)

The Commission recommends the distribution of net tax proceeds between the Union and the States and determines the allocation among States.

It also lays down principles governing grants-in-aid from the Consolidated Fund of India, suggests measures to strengthen State resources for Panchayats and Municipalities, and considers any additional fiscal matter referred by the President in the interest of sound public finance.

Presentation of report to Parliament

Article 281 requires the President to place the Commission’s report before both Houses of Parliament, along with an explanatory memorandum detailing the action taken.

Constitutional provisions on tax sharing and grants

Article 270 provides the basis for sharing Union taxes with States through a divisible pool, the distribution of which is recommended by the Commission.

Article 275 empowers Parliament to provide grants-in-aid from the Consolidated Fund of India based on the Commission’s recommendations.

Articles 243H and 243X enable States to authorise Panchayats and Municipalities to levy taxes and receive grants, with the Commission suggesting measures to augment these resources.

All grants are charged to the Consolidated Fund of India under Article 266.

Statutory framework and presidential reference

The Finance Commission (Miscellaneous Provisions) Act, 1951, enacted under Article 280(1), prescribes the qualifications, tenure, and service conditions of members.

Additionally, the President may refer supplementary fiscal issues to the Commission beyond those expressly mentioned in the Constitution.

Overview of the Sixteenth Finance Commission

The Sixteenth Finance Commission, chaired by Dr. Arvind Panagariya, submitted its report covering the period from 2026–27 to 2030–31. The report was tabled in Parliament on February 1, 2026.

Tax Devolution Framework

Share of States in central taxes: The Commission has recommended that 41 percent of the divisible pool of central taxes be allocated to States, maintaining the same share as suggested by the Fifteenth Finance Commission.

The divisible pool is calculated after deducting collection costs, cesses, and surcharges from the gross tax revenue of the Union government.

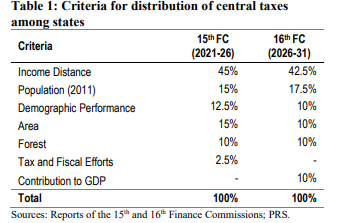

Criteria for horizontal devolution: To distribute tax proceeds among States, the Commission adopted a formula assigning weight to specific parameters.

Per Capita GSDP Distance Income Distance: Income distance is defined as the gap between a State’s per capita Gross State Domestic Product and the average per capita GSDP of the three largest States with the highest per capita income.

The calculation uses the average for 2018–19 to 2023–24, excluding 2020–21. States with lower per capita GSDP receive a larger share to promote equity.

Population criterion: Population share is based on data from the 2011 Census and determines allocation under this parameter.

Demographic performance: The Commission revised this parameter to reflect population growth between 1971 and 2011 instead of changes in Total Fertility Rate. States exhibiting lower population growth are rewarded with a higher share.

Forest and ecological considerations: Weight has been assigned to both the proportion of total forest area in a State and the increase in forest area between 2015 and 2023. Open forests are included in the calculation.

This marks a departure from the previous Commission, which considered only dense and moderately dense forests and focused solely on overall share.

Contribution to GDP: A new parameter accounts for States’ contribution to national output. It replaces the earlier tax and fiscal effort criterion.

Contribution is computed as the square root of a State’s GSDP divided by the sum of square roots of GSDPs of all States, based on average nominal GSDP from 2018–19 to 2023–24, excluding 2020–21.

Grants in Aid Structure

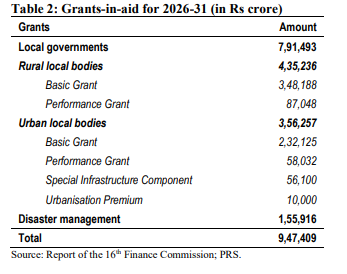

Overall grants recommendation: The Commission has recommended grants amounting to Rs 9.47 lakh crore over five years.

These include allocations for local bodies and disaster management. Revenue deficit, sector-specific, and state-specific grants have been discontinued.

Local Body Grants

- Allocation for rural and urban bodies: Grants of Rs 4.4 lakh crore and Rs 3.6 lakh crore have been recommended for rural and urban local bodies, respectively. Eighty percent constitutes basic grants and twenty percent performance-based grants.

- Entry level conditions: Release of funds is conditional upon constitutional constitution of local bodies, publication of provisional and audited accounts, and timely formation of State Finance Commissions.

- Basic grants structure: Half of the basic grants remain untied, while the remaining half is earmarked for sanitation, solid waste management, and water management.

- Performance grants structure: Performance grants comprise state-level and local body-level components. States must meet benchmarks for transferring their own resources to local bodies. Local bodies must achieve specified targets in own-source revenue growth.

- Special infrastructure grants: This component supports comprehensive wastewater management systems in cities with populations between 10 and 40 lakh as per the 2011 Census. A total of Rs 56,100 crore has been allocated.

- Urbanisation premium grant: A one-time grant of Rs 10,000 crore has been proposed for merging peri-urban villages with adjacent urban bodies and for framing a Rural to Urban Transition Policy.

Disaster Management Grants

Corpus and cost sharing: A total corpus of Rs 2,04,401 crore has been recommended for State Disaster Relief and Management Funds.

The sharing ratio is 90:10 for northeastern and Himalayan States and 75:25 for others. The Centre’s contribution amounts to Rs 1,55,916 crore.

Fiscal Consolidation Roadmap

- Targets for fiscal deficit: The Centre is advised to reduce its fiscal deficit to 3.5 percent of GDP by 2030–31. States are recommended to adhere to an annual fiscal deficit limit of 3 percent of GSDP.

- Off budget borrowings: The Commission has urged discontinuation of off-budget borrowings and their inclusion in formal budgetary accounts. Definitions of fiscal deficit and debt should uniformly incorporate such liabilities.

- Debt trajectory: Combined debt of the Union and States is projected to decline from 77.3 percent of GDP in 2026–27 to 73.1 percent by 2030–31.

Power Sector Reforms

- Privatisation of distribution companies: States are encouraged to pursue privatisation of electricity distribution companies. A special purpose vehicle may be created to absorb legacy debt, protecting private investors from inherited liabilities.

- Utilisation of special assistance: Debt repayment through the Special Assistance Scheme for Capital Investment is permitted only after completion of the privatisation process.

Subsidy Rationalisation

- Review and targeting of subsidies: States are advised to reassess and rationalise subsidy expenditure, particularly unconditional cash transfers that may lack effective targeting. Clear exclusion criteria and systematic reviews are recommended.

- Accounting and transparency reforms: Financing subsidies through off-budget borrowings should cease. A standardised framework for defining, accounting, and disclosing subsidies and transfers across States is recommended to prevent misclassification.

Public Sector Enterprise Reforms

- Closure and disinvestment strategy: The Commission has proposed reviewing and closing 308 inactive State Public Sector Enterprises. States should adopt disinvestment policies targeting non-performing entities.

- Loss making enterprises oversight: Enterprises incurring losses in three of four consecutive years should be placed before the Cabinet for decisions regarding closure, privatisation, or continuation based on strategic considerations.